Sun Pharma shares rose 7% after announcing an $11.75 billion deal to acquire U.S.-based Organon, expanding its global footprint.

By Emma Clarke | Edited by Oleg Petrenko

Published:

Updated:

Sun Pharma shares climbed 7% after announcing an $11.75 billion acquisition of U.S.-based Organon, expanding its global footprint. Photo: Sun Pharma / X

Sun Pharmaceutical Industries shares jumped approximately 7% after the company announced plans to acquire U.S.-based Organon & Co. in an all-cash deal valued at $11.75 billion.

The acquisition marks a major step in Sun Pharma’s global expansion strategy, significantly increasing its presence in the U.S. pharmaceutical market and strengthening its portfolio across key therapeutic areas.

Organon, headquartered in New Jersey, focuses on women’s health, biosimilars, and established medicines, offering Sun Pharma access to a diversified and globally recognized product base.

Strategic Acquisition Expands Global Reach

The deal is aimed at accelerating Sun Pharma’s international growth by leveraging Organon’s established footprint in developed markets.

By combining operations, the company expects to benefit from expanded distribution networks, increased scale, and enhanced research and development capabilities.

Management highlighted the strategic fit between the two businesses, noting that Organon’s product lineup complements Sun Pharma’s existing portfolio and opens new revenue streams.

As previously covered, cross-border acquisitions have become a key growth strategy for pharmaceutical companies seeking to diversify and access new markets.

The all-cash structure of the transaction underscores Sun Pharma’s confidence in the long-term value of the acquisition.

Market Reaction Reflects Investor Confidence in Expansion Strategy

The positive reaction in Sun Pharma’s stock suggests that investors view the acquisition as a value-accretive move that could strengthen the company’s competitive position.

Analysts point to potential synergies, including cost efficiencies and revenue growth opportunities, as key drivers of long-term value.

At the same time, the deal introduces execution risks, including integration challenges and regulatory approvals across multiple jurisdictions.

The pharmaceutical sector remains highly competitive, with companies increasingly pursuing consolidation to scale operations and manage rising development costs.

For markets, the transaction highlights a broader trend of global expansion and consolidation within the healthcare industry, as companies position themselves for sustained growth.

Sun Pharma’s ability to successfully integrate Organon and realize projected benefits will be a key factor shaping investor sentiment in the coming quarters.

Microsoft is introducing its first voluntary buyout program, targeting up to 7% of its U.S. workforce as part of broader efficiency efforts.

By Emma Clarke | Edited by Oleg Petrenko

Published:

Microsoft is rolling out its first voluntary buyout program, covering up to 7% of its U.S. workforce as part of broader efficiency efforts. Photo: Angel Bena / Pexels

Microsoft is planning its first-ever voluntary employee buyout program, offering exit packages to eligible U.S. workers as part of a broader push to streamline operations and manage costs.

The program could affect up to 7% of the company’s U.S. workforce and will be available to employees at the senior director level and below whose combined age and years of service total at least 70.

The move marks a shift in Microsoft’s workforce strategy, as the company looks to balance ongoing investments in artificial intelligence with operational efficiency.

Buyout Program Targets Cost Control Amid AI Spending

The voluntary buyout initiative reflects increasing pressure on major technology companies to control costs while maintaining aggressive investment in AI infrastructure and development.

Microsoft has been ramping up spending on data centers, cloud computing, and AI platforms, positioning itself as a leader in enterprise AI solutions.

By offering voluntary exits instead of mandatory layoffs, the company aims to reduce headcount in a more controlled and less disruptive manner.

As previously covered, tech firms have increasingly turned to workforce optimization strategies as they scale AI investments and adjust to shifting market conditions.

The eligibility criteria suggest the program is focused on more experienced employees, potentially reshaping the company’s workforce composition over time.

Market Implications Highlight Big Tech Efficiency Focus

The announcement underscores a broader trend across Big Tech, where companies are prioritizing cost discipline alongside long-term growth initiatives.

Investors have generally responded positively to such measures, viewing them as a way to protect margins and improve capital allocation.

At the same time, the move signals that even highly profitable companies like Microsoft are reassessing staffing levels in response to changing technological and economic dynamics.

Analysts note that voluntary programs may reduce reputational risks compared to layoffs, while still achieving meaningful cost savings.

For markets, the development reinforces a key theme: the AI investment cycle is reshaping corporate strategies, driving both innovation and structural changes in workforce management.

Microsoft’s approach will be closely watched as an example of how companies navigate the balance between growth and efficiency in the evolving tech landscape.

TSMC shares reached a record high after Taiwan eased single-stock investment caps, boosting demand from institutional funds.

By Daniel Wright | Edited by Oleg Petrenko

Published:

TSMC shares hit a record high after Taiwan relaxed single-stock investment caps, driving increased demand from institutional funds. Photo: 4300streetcar / Wikimedia

Shares of Taiwan Semiconductor Manufacturing Company climbed to a record high after regulators eased restrictions on how much institutional funds can invest in a single stock, unlocking additional demand for one of the world’s most valuable chipmakers.

The rally follows a strong earnings report, with TSMC posting a 58% year-over-year increase in first-quarter profit, driven by robust demand for advanced chips used in artificial intelligence and high-performance computing.

The policy change allows funds greater flexibility to allocate capital to top-performing companies, a move that has disproportionately benefited large-cap leaders like TSMC.

Policy Shift Boosts Institutional Demand for Chip Giant

Taiwan’s decision to relax single-stock investment caps is expected to channel more capital into leading domestic companies, particularly those with strong growth prospects and global relevance.

TSMC, as the dominant contract chip manufacturer globally, stands out as a primary beneficiary, given its critical role in supplying advanced semiconductors to major technology firms.

The easing of limits effectively removes a structural constraint that previously capped exposure, enabling funds to increase their positions in high-conviction names.

As previously covered, regulatory changes can have a significant impact on capital flows, particularly in markets where institutional allocation rules play a key role in shaping demand.

The move also reflects broader efforts by Taiwan to strengthen its capital markets and support key industries such as semiconductors.

The surge in TSMC shares underscores continued strength in the semiconductor sector, fueled by rising demand for AI-related hardware.

Investors are increasingly focused on companies that provide the infrastructure for AI development, including advanced chip manufacturing and design.

TSMC’s strong earnings performance reinforces its position as a core beneficiary of this trend, with sustained demand from clients across cloud computing, data centers, and consumer electronics.

At the same time, the record-high valuation raises questions about how much of the AI-driven growth is already priced into the stock.

For markets, the development highlights a key theme: policy support and structural demand are converging to drive momentum in the semiconductor sector.

TSMC’s performance will continue to serve as a benchmark for investor sentiment toward the broader AI and technology ecosystem.

OpenAI released GPT-5.5 with improved efficiency and a focus on agentic coding, though higher pricing reflects its expanded capabilities.

By Daniel Wright | Edited by Oleg Petrenko

Published:

OpenAI launched GPT-5.5 with enhanced efficiency and a focus on agentic coding, while higher pricing reflects its expanded capabilities. Photo: OpenAI

OpenAI has unveiled GPT-5.5, its latest model designed with a strong focus on agentic coding and real-world productivity, as competition intensifies in the rapidly evolving artificial intelligence market.

The new model introduces improved efficiency, requiring fewer tokens to deliver high-quality outputs, a key metric for developers and enterprises seeking to optimize performance and cost.

However, the pricing has increased, with API costs set at approximately $5 per million input tokens and $30 per million output tokens. The Pro tier is priced significantly higher at $30 and $180 respectively, reflecting the model’s enhanced capabilities.

Efficiency Gains and Coding Focus Drive Product Upgrade

GPT-5.5 is positioned as a model built for “real work”, with enhanced capabilities in coding, scientific research, and enterprise-level tasks.

A major improvement lies in its ability to achieve better results with fewer tokens, which can reduce computational overhead and improve overall system efficiency despite higher per-token pricing.

The emphasis on agentic coding reflects a broader industry trend, where AI systems are increasingly expected to operate autonomously across complex workflows rather than simply generate text.

The model is available to a wide range of users, including subscribers to Plus, Pro, Business, and Enterprise plans, signaling OpenAI’s intent to scale adoption across both individual and corporate segments.

As previously covered, AI developers are racing to improve both performance and efficiency as demand for large-scale deployment continues to grow.

Market Implications Highlight Pricing Power and Competitive Pressure

The launch underscores OpenAI’s strategy to balance technological advancement with monetization, as it continues to invest heavily in infrastructure and model development.

Higher pricing suggests confidence in the model’s value proposition, particularly for enterprise users willing to pay for improved performance and reliability.

At the same time, competition remains intense, with companies like Google and Anthropic advancing their own models and pushing innovation across the sector.

For investors and industry observers, the key question is whether efficiency gains can offset rising costs and drive broader adoption.

The focus on agentic capabilities also signals a shift toward AI systems that can perform tasks independently, potentially transforming productivity across industries.

GPT-5.5’s rollout reinforces a central theme in the AI market: innovation is accelerating, but so are the economic and competitive stakes shaping the future of the industry.

Tesla has started Cybercab production in Texas without volume restrictions, signaling a major step in scaling its autonomous vehicle strategy.

By Oleg Petrenko

Published:

Tesla has begun Cybercab production in Texas without volume limits, marking a key step in scaling its autonomous vehicle strategy. Photo: Tesla / X

Tesla has officially begun production of its Cybercab autonomous vehicle in Texas, marking a significant milestone in its push to scale robotaxi services without traditional volume constraints.

The company confirmed that production is underway despite ongoing delays in fully unsupervised driving capabilities, with executives indicating that the program is moving forward under a self-certification framework.

Notably, the Cybercab is not subject to the U.S. National Highway Traffic Safety Administration’s typical 2,500-vehicle exemption cap, allowing Tesla to scale production more aggressively.

Tesla’s decision to rely on self-certification allows it to bypass certain regulatory limitations that typically restrict the number of autonomous vehicles deployed during early testing phases.

This approach could significantly accelerate the rollout of its robotaxi fleet, particularly if the company is able to demonstrate safety and reliability at scale.

The Cybercab is designed as a purpose-built autonomous vehicle, with no traditional driver controls, reflecting Tesla’s long-term vision of fully driverless transportation.

As previously covered, Tesla has been positioning its robotaxi strategy as a core growth driver, aiming to generate recurring revenue through ride-hailing services.

The launch in Texas builds on earlier deployments in cities such as Austin, reinforcing the state as a central hub for Tesla’s autonomous vehicle development.

Market Implications Highlight Growth Potential and Regulatory Risks

The start of production without volume limits is likely to be viewed as a bullish signal by investors, indicating that Tesla is moving closer to large-scale commercialization of its autonomous platform.

However, the reliance on self-certification also raises regulatory and safety concerns, particularly as authorities continue to evaluate frameworks for autonomous vehicles.

Competition in the robotaxi space is intensifying, with players such as Waymo and other technology firms advancing their own driverless solutions.

For investors, the key question is whether Tesla can successfully scale its Cybercab network while navigating regulatory scrutiny and maintaining safety standards.

The development underscores a broader market theme: autonomous driving remains one of the most high-stakes and potentially transformative segments within the AI and mobility landscape.

Tesla’s progress in this area will be closely watched as an indicator of how quickly robotaxi services can transition from pilot programs to mainstream adoption.

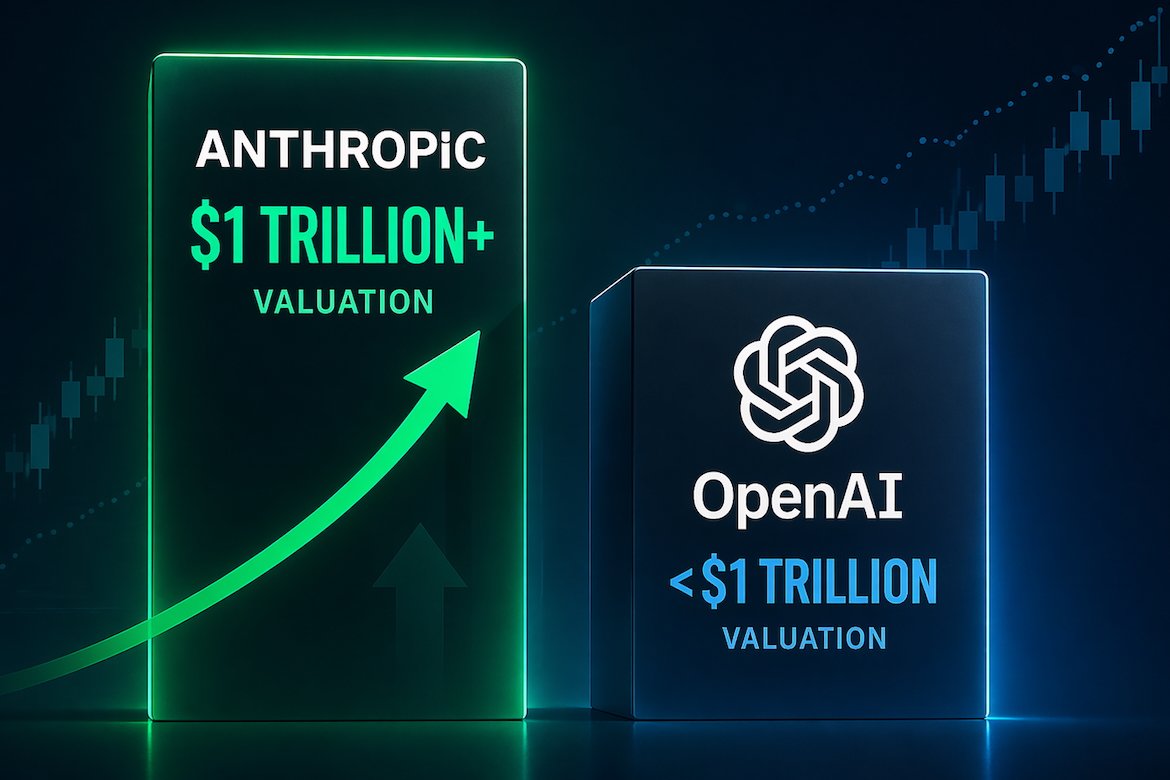

Anthropic is trading at a $1 trillion valuation on secondary markets, surpassing OpenAI and highlighting shifting investor sentiment in AI.

By Daniel Wright | Edited by Oleg Petrenko

Published:

Anthropic is valued at around $1 trillion on secondary markets, surpassing OpenAI and reflecting shifting investor sentiment in the AI sector. Photo: Oleg Petrenko / MarketSpeaker

Anthropic is being valued at approximately $1 trillion on secondary markets, surpassing OpenAI and marking a significant shift in investor sentiment within the artificial intelligence sector.

Shares of Anthropic on platforms such as Forge Global have surged sharply, pushing the company’s implied valuation well above its most recent funding round just three months ago, when it was valued at around $380 billion.

In contrast, OpenAI is currently trading at an estimated $880 billion on the same secondary market, only slightly above its last primary funding valuation.

Secondary Market Surge Reflects Changing AI Leadership Narrative

The sharp increase in Anthropic’s valuation underscores growing investor confidence in the company’s positioning within the AI ecosystem.

Secondary markets often act as an early signal of shifting sentiment, particularly for high-profile private companies where access to shares is limited.

Anthropic’s rapid valuation expansion suggests strong demand for exposure to its AI models and infrastructure, as investors look for alternatives to more established players.

As previously covered, capital has been flowing aggressively into AI companies, driving valuations higher across both public and private markets.

The divergence between Anthropic and OpenAI valuations may reflect differences in perceived growth potential, strategic partnerships, and product positioning.

Market Implications Highlight Intensifying Competition in AI

The development highlights how quickly leadership dynamics in the AI sector can shift as companies compete for talent, capital, and technological breakthroughs.

Investors are increasingly evaluating firms not just on current capabilities, but on long-term scalability and monetization potential.

The rise of secondary market valuations also reflects limited access to primary funding rounds, pushing investors to seek exposure through alternative channels.

However, analysts caution that secondary market pricing can be more volatile and less transparent than traditional funding rounds.

For markets, the shift underscores a broader theme: the AI race is entering a new phase where valuation leadership is fluid and closely tied to investor expectations.

Anthropic’s surge past the $1 trillion mark signals both the scale of opportunity in AI and the intensity of competition shaping the sector’s future.

FTX’s investment portfolio could be worth $114 billion today if assets hadn’t been sold during its 2022 collapse, driven by massive gains in AI and tech holdings.

By David Sinclair | Edited by Oleg Petrenko

Published:

Updated:

FTX’s investment portfolio could be valued at around $114 billion today if its assets hadn’t been liquidated during the 2022 collapse, fueled by sharp gains in AI and tech holdings. Photo: Oleg Petrenko / MarketSpeaker

FTX’s investment portfolio could have been worth approximately $114 billion today had its assets not been liquidated following the company’s collapse in 2022, according to estimates based on current valuations.

At the time of its bankruptcy, administrators moved quickly to sell off holdings to repay creditors, effectively locking in losses and forfeiting exposure to what has since become one of the strongest rallies in technology and artificial intelligence assets.

The missed upside highlights the dramatic surge in valuations across AI, crypto, and private tech companies over the past two years.

AI and Tech Holdings Drove Massive Hypothetical Gains

A significant portion of the unrealized gains would have come from investments in artificial intelligence and high-growth technology companies.

Anthropic alone would account for approximately $82.3 billion of the total, reflecting a roughly 165x increase in value. SpaceX holdings could be worth around $15 billion, representing a 75x gain.

Other positions include Cursor at an estimated $3 billion an extraordinary 15,000x return along with Robinhood at $4.9 billion (8x) and Genesis Digital at $3.5 billion (3x).

FTX also held a substantial position in Solana, now valued at approximately $5.1 billion, reflecting a 27x increase since the liquidation period.

As previously covered, the AI boom has driven unprecedented capital inflows into both public and private markets, significantly boosting valuations across the sector.

Market Lessons Highlight Timing and Forced Liquidation Risks

The case underscores the impact of forced liquidation during periods of market stress, where assets are often sold at depressed valuations to meet immediate obligations.

While the strategy helped repay creditors, it eliminated exposure to long-term growth themes that later delivered outsized returns.

Analysts note that such scenarios are common in financial crises, where liquidity pressures override investment horizons.

For investors, the example reinforces the importance of balance sheet resilience and risk management, particularly in volatile markets.

At the same time, the scale of the hypothetical gains reflects broader market dynamics, including the rapid expansion of AI valuations and the recovery of risk assets following the downturn.

The FTX case serves as a stark illustration of how timing, leverage, and liquidity constraints can significantly influence long-term investment outcomes.

Meta plans to cut about 10% of its workforce, or over 8,000 jobs, as it streamlines operations and offsets rising AI-related costs.

By Emma Clarke | Edited by Oleg Petrenko

Published:

Meta plans to reduce its workforce by about 10%, or more than 8,000 jobs, as it streamlines operations and offsets rising AI-related costs. Photo: Dima Solomin / Unsplash

Meta Platforms is planning to cut approximately 10% of its workforce – more than 8,000 employees – as part of a broader effort to improve efficiency and manage rising costs tied to its aggressive investments in artificial intelligence.

The company will also eliminate around 6,000 open roles, signaling a significant slowdown in hiring alongside the workforce reduction. The move underscores a shift toward tighter cost controls as Meta continues to allocate substantial resources to AI infrastructure and product development.

Meta accounts for roughly 2.4% of the S&P 500’s total market capitalization, making the restructuring a notable development for broader equity markets.

Cost Cuts Reflect Pressure From AI Investment Cycle

The layoffs highlight the financial strain created by large-scale investments in AI, including data centers, chips, and advanced software development.

Meta has been ramping up spending to compete with other technology giants in building next-generation AI capabilities, particularly in generative AI and infrastructure.

By reducing headcount and freezing hiring, the company aims to offset these expenses and improve operating efficiency without slowing its long-term strategic initiatives.

As previously covered, major tech firms have increasingly balanced aggressive AI spending with cost discipline, often through layoffs and operational restructuring.

The decision also reflects a broader industry trend, where companies are reassessing workforce needs as automation and AI tools enhance productivity.

Market Implications Highlight Big Tech Cost Discipline

The restructuring is likely to be viewed positively by investors, who have increasingly rewarded technology companies for demonstrating financial discipline alongside growth investments.

Cost reductions could support margins and free up capital for continued AI expansion, reinforcing Meta’s position in the competitive tech landscape.

At the same time, the scale of the layoffs underscores the intensity of the AI investment cycle and its impact on corporate strategy.

Analysts note that Meta’s size and weight in major indices amplify the significance of its decisions, with potential implications for overall market sentiment.

For investors, the key question is whether Meta can successfully translate its AI spending into revenue growth while maintaining profitability.

The company’s ability to balance innovation with cost control will remain a central focus in the coming quarters, particularly as competition in the AI space continues to intensify.

Warner Bros. Discovery shareholders approved a $110 billion merger with Paramount, advancing one of the largest media consolidation deals in recent years.

By Emma Clarke | Edited by Oleg Petrenko

Published:

Warner Bros. Discovery shareholders approved a $110 billion merger with Paramount, moving forward one of the largest media consolidation deals in recent years. Photo: Oleg Petrenko / MarketSpeaker

Warner Bros. Discovery shareholders have approved the company’s $110 billion merger with Paramount, clearing a key hurdle for one of the largest consolidation deals in the global media industry.

The vote paves the way for the combination of two major entertainment companies, as they seek to strengthen their position in an increasingly competitive streaming landscape dominated by global platforms.

The deal, which also involves Skydance Media, is expected to reshape the competitive dynamics of the sector by combining content libraries, production capabilities, and distribution networks.

Strategic Merger Aims to Strengthen Streaming and Content Scale

The merger reflects growing pressure on traditional media companies to scale up in order to compete with streaming giants and technology platforms.

By combining Warner Bros. Discovery’s extensive portfolio with Paramount’s content assets, the new entity aims to enhance its ability to attract subscribers and compete globally.

Executives have emphasized potential synergies, including cost savings, improved content distribution, and stronger negotiating power with advertisers and partners.

As previously covered, consolidation has become a defining trend in the media industry, as companies seek to balance rising content costs with the need to expand their audience reach.

The involvement of Skydance Media further strengthens the production pipeline, adding to the combined company’s ability to deliver high-profile film and television projects.

Market Implications Highlight Ongoing Media Industry Consolidation

The approval underscores a broader shift toward consolidation as companies respond to changing consumer behavior and intensifying competition.

Investors are closely watching whether the combined entity can achieve the expected synergies and deliver sustainable growth in a challenging market environment.

The streaming sector has faced slowing subscriber growth and increasing profitability pressures, prompting companies to explore strategic combinations.

At the same time, large-scale mergers carry execution risks, including integration challenges and potential regulatory scrutiny.

For markets, the deal highlights a key theme: scale is becoming increasingly critical in the media and entertainment industry, particularly as content costs rise and competition intensifies.

The success of the Warner Bros. Discovery–Paramount combination will likely influence future consolidation moves across the sector.

American Airlines lowered its 2026 earnings forecast as rising jet fuel prices significantly increased operating costs.

By Nathan Cole | Edited by Oleg Petrenko

Published:

American Airlines cut its 2026 earnings outlook as higher jet fuel prices significantly increased operating costs. Photo: Ross Sokolovski / Unsplash

American Airlines has cut its 2026 earnings projections, becoming the latest carrier to revise its outlook as a sharp rise in jet fuel costs adds significant pressure to operating expenses.

The company said higher fuel prices have added billions of dollars to its cost base, prompting a reassessment of its financial expectations for the coming year. The warning reflects broader challenges across the airline industry, where fuel remains one of the largest and most volatile expenses.

Shares moved lower following the announcement, as investors reacted to the weaker outlook and growing concerns over margin compression.

Fuel Price Surge Drives Cost Pressures Across Airlines

The increase in jet fuel prices has been driven in part by geopolitical tensions, particularly in the Middle East, which have disrupted energy markets and pushed oil prices higher.

For airlines, even modest increases in fuel costs can have an outsized impact on profitability, given the scale of consumption and limited ability to hedge against volatility in the short term.

American Airlines noted that the surge in fuel expenses is expected to outweigh gains from strong travel demand, highlighting the delicate balance between revenue growth and cost management.

As previously covered, multiple carriers have recently flagged similar concerns, underscoring a sector-wide challenge as fuel prices remain elevated.

The situation is particularly acute for U.S. airlines, which are highly sensitive to fluctuations in energy markets and face intense competition that limits pricing flexibility.

Market Reaction Reflects Broader Sector Risks

The downgrade in American Airlines’ outlook highlights investor concerns about the sustainability of earnings in the airline sector under current cost conditions.

Higher fuel prices not only reduce margins but also constrain airlines’ ability to offer competitive ticket pricing without eroding profitability.

Analysts note that while demand for travel remains relatively strong, rising input costs could offset much of the benefit, leading to weaker overall financial performance.

At the same time, geopolitical uncertainty continues to add volatility, making it difficult for airlines to plan capacity and pricing strategies effectively.

For investors, the key question is whether airlines can adapt through cost controls, efficiency improvements, or pricing adjustments, or if margins will remain under pressure in the near term.

The outlook for the sector will likely depend heavily on the trajectory of oil prices and the broader macroeconomic environment, both of which remain uncertain.

Netflix approved an additional $25 billion share buyback program, signaling a renewed focus on shareholder returns after abandoning a major acquisition plan.

By Emma Clarke | Edited by Oleg Petrenko

Published:

Netflix authorized an additional $25 billion share buyback program, signaling a renewed emphasis on returning capital to shareholders after dropping a major acquisition plan. Photo: Anastasia Shuraeva / Pexels

Netflix has authorized an additional $25 billion share buyback program, marking a significant step toward returning capital to shareholders following its decision to abandon a major acquisition effort.

The new authorization comes on top of an existing buyback plan approved in December 2024, which still had approximately $6.8 billion remaining as of the end of March.

Shares rose modestly in premarket trading after the announcement, reflecting investor support for the move as the company pivots away from large-scale mergers and acquisitions.

Capital Return Strategy Follows Abandoned Acquisition Plans

The buyback decision follows Netflix’s withdrawal from a proposed $72 billion deal to acquire assets from Warner Bros. Discovery, a move that had previously weighed on the stock.

By shifting toward share repurchases, the company is signaling confidence in its financial position and long-term cash generation.

The new program has no expiration date, giving Netflix flexibility in how and when it executes repurchases depending on market conditions.

As previously covered, companies often increase buybacks after stepping back from large acquisitions, reallocating capital toward shareholder returns instead of external growth.

Netflix is also continuing to invest heavily in content and platform expansion, with expectations to spend roughly $20 billion annually on films and television production.

The $25 billion authorization underscores a broader strategic pivot, as Netflix balances growth initiatives with capital discipline.

Investors are likely to view the move as supportive for the stock, particularly after recent volatility tied to earnings expectations and strategic uncertainty.

At the same time, analysts note that the buyback does not fully clarify how Netflix plans to allocate capital for long-term growth beyond content and platform investments.

The company has been expanding into new areas such as advertising, live programming, and gaming, all of which could influence future revenue streams.

For markets, the development reflects a familiar theme: major tech companies are increasingly using buybacks to stabilize valuations and signal confidence amid shifting strategic priorities.

Netflix’s ability to combine capital returns with sustained growth will remain a key factor for investor sentiment in the coming quarters.

Nvidia backed AI infrastructure firm Vast Data in a funding round valuing the company at $30 billion, highlighting strong demand for AI data solutions.

By Daniel Wright | Edited by Oleg Petrenko

Published:

Updated:

Nvidia invested in AI infrastructure firm Vast Data in a funding round that valued the company at $30 billion, underscoring strong demand for AI data solutions. Photo: Coolcaesar / Wikimedia

Nvidia has backed AI infrastructure company Vast Data in a new funding round that values the firm at $30 billion, underscoring continued investor appetite for companies powering the artificial intelligence boom.

The New York-based company raised approximately $1 billion in its latest financing, more than tripling its valuation from around $9.1 billion in 2023.

Vast Data develops software that enables enterprises to manage and process large-scale datasets used in AI training and operations, positioning it as a critical player in the expanding AI infrastructure ecosystem.

AI Infrastructure Demand Drives Valuation Surge

The sharp increase in valuation reflects surging demand for data infrastructure as companies scale AI workloads across cloud platforms and data centers.

Vast Data’s technology is designed to handle massive volumes of information efficiently, enabling faster data access for AI models and high-performance computing systems.

Its client base includes major players such as xAI and CoreWeave, highlighting its role in supporting some of the most advanced AI deployments globally.

The funding round was led by Drive Capital and Access Industries, with participation from existing investors including Nvidia, as well as firms like Fidelity and NEA.

As previously covered, infrastructure providers are increasingly seen as essential beneficiaries of the AI boom, often capturing value alongside chipmakers and cloud platforms.

Market Implications Highlight Expanding AI Ecosystem

Nvidia’s continued investment activity reflects a broader strategy of backing companies across the AI value chain rather than focusing solely on its core chip business.

By supporting firms like Vast Data, Nvidia strengthens its ecosystem, ensuring that demand for its GPUs is complemented by robust data infrastructure and software platforms.

Investors are increasingly targeting these “picks and shovels” companies that enable AI development, viewing them as critical to sustaining long-term growth in the sector.

At the same time, the rapid rise in valuations has sparked debate over whether AI-related assets are becoming overheated, particularly as capital flows accelerate.

For markets, the deal reinforces a key theme: the AI boom is not limited to model developers or chipmakers but extends across a broad network of infrastructure providers.

Vast Data’s trajectory will be closely watched as a potential indicator of how much value the market assigns to the underlying systems powering artificial intelligence.

Condom prices could increase by up to 30% as the Iran war drives higher costs and disrupts supply chains, according to global producer Karex.

By Nathan Cole | Edited by Oleg Petrenko

Published:

Condom prices may rise by up to 30% as the Iran war increases costs and disrupts global supply chains, according to leading producer Karex. Photo: Nataliya Vaitkevich / Pexels

Global condom prices could rise by as much as 30% as the Iran war drives up costs and disrupts supply chains, according to Karex, the world’s largest manufacturer of condoms.

The Malaysia-based company, which produces more than 5 billion units annually and supplies major brands such as Durex and Trojan, warned that geopolitical tensions are already impacting raw material costs, logistics, and currency dynamics.

The expected price increase highlights how the conflict is extending beyond energy markets into consumer goods, affecting even essential healthcare products.

Rising Costs and Supply Chain Disruptions Drive Price Pressure

Karex said the Iran war has contributed to higher transportation costs and increased volatility in raw material pricing, particularly for latex, a key input in condom production.

Energy prices, which influence manufacturing and shipping expenses, have also been affected by the conflict, adding further pressure on margins.

Currency fluctuations in emerging markets are compounding the issue, making imports more expensive and increasing overall production costs.

As previously covered, geopolitical tensions in the Middle East have had ripple effects across global supply chains, impacting industries far beyond oil and gas.

The company indicated that price adjustments may be necessary to offset rising costs, with increases potentially passed on to distributors and consumers.

The potential price surge underscores how geopolitical shocks can feed into broader inflationary pressures, even in sectors typically considered stable.

Higher prices for basic healthcare products could have wider social implications, particularly in developing markets where affordability is a key concern.

For investors, the development signals ongoing supply chain fragility and cost volatility, themes that have persisted across global markets in recent years.

Companies operating in consumer goods sectors may face similar challenges, balancing cost increases with pricing strategies in a sensitive demand environment.

The situation also reinforces a broader market trend: geopolitical risks are increasingly influencing pricing dynamics across a wide range of industries.

As the conflict evolves, analysts expect continued volatility in both commodity prices and downstream consumer goods, with potential implications for inflation and corporate margins globally.

Quantinuum, Honeywell’s quantum computing unit, has confidentially filed for a U.S. IPO, signaling growing investor interest in next-generation computing.

By Daniel Wright | Edited by Oleg Petrenko

Published:

Updated:

Quantinuum, Honeywell’s quantum computing division, has confidentially filed for a U.S. IPO, highlighting rising investor interest in next-generation computing. Photo: Oleg Petrenko / MarketSpeaker

Quantinuum, the quantum computing unit backed by Honeywell, has confidentially filed for an initial public offering in the United States, marking a significant step toward bringing one of the sector’s leading players to public markets.

The confidential filing allows the company to move forward with IPO preparations while keeping key financial details private until later stages of the process. Timing and valuation have not yet been disclosed.

The move comes amid growing investor interest in quantum computing, as advances in artificial intelligence and high-performance computing drive demand for next-generation technologies.

Quantum Computing Push Gains Momentum Ahead of IPO Wave

Quantinuum is considered one of the more advanced players in the quantum computing space, focusing on both hardware and software solutions designed to solve complex computational problems.

The company has been positioning itself at the forefront of the industry, targeting applications in areas such as cybersecurity, materials science, and drug discovery.

Its backing by Honeywell provides both financial support and industrial expertise, strengthening its credibility in a sector that remains highly technical and capital-intensive.

As previously covered, quantum computing has increasingly attracted investor attention as a long-term growth opportunity, particularly as breakthroughs in AI and computing accelerate interest in alternative processing architectures.

The confidential IPO filing suggests that Quantinuum is seeking to capitalize on favorable market conditions, including strong demand for emerging technology listings.

Market Implications Highlight Rising Interest in Advanced Computing

The planned IPO underscores a broader trend of capital flowing into advanced computing sectors, including quantum technology, AI infrastructure, and semiconductors.

Investors are increasingly looking for exposure to next-generation technologies that could reshape industries over the coming decades.

However, the quantum computing sector remains in an early stage, with limited near-term revenue visibility and significant technical challenges still to overcome.

Analysts caution that valuations in the space may reflect long-term potential rather than immediate financial performance.

For markets, Quantinuum’s IPO will serve as a key test of investor appetite for quantum computing companies, particularly as part of a broader wave of technology listings expected in 2026.

The outcome could influence how future advanced computing firms approach public markets and capital raising strategies.

Nvidia and Google announced a major partnership to develop AI infrastructure, combining hardware and software to advance ‘physical’ and agentic AI systems.

By Daniel Wright | Edited by Oleg Petrenko

Published:

Updated:

Nvidia and Google unveiled a major partnership to build AI infrastructure, integrating hardware and software to advance 'physical' and agentic AI systems. Photo: Oleg Petrenko / MarketSpeaker

Nvidia and Google have announced a sweeping partnership aimed at advancing both software and hardware capabilities in artificial intelligence, with a focus on building large-scale “AI factories” to support next-generation computing.

The collaboration combines Nvidia’s latest GPU architecture including Blackwell and Rubin systems with Google Cloud’s infrastructure and Gemini AI models, enabling enterprises to develop and deploy advanced AI applications at unprecedented scale.

The initiative reflects growing demand for integrated AI ecosystems, where computing power, software models, and cloud infrastructure work together seamlessly.

Partnership Targets Next Wave of AI Infrastructure

At the core of the partnership is the concept of “AI factories” – massive computing environments designed to train and deploy increasingly complex AI systems.

The companies said these systems will support both “agentic AI”, capable of autonomous decision-making, and “physical AI”, which integrates intelligence into real-world systems such as robotics and industrial automation.

Google Cloud will offer distributed infrastructure powered by Nvidia GPUs, including configurations that can scale to nearly one million Rubin GPUs, significantly expanding computing capacity for enterprise clients.

The partnership also integrates Nvidia’s AI software stack, including NeMo and Nemotron models, with Google’s Gemini platform, creating a unified environment for developers.

As previously covered, demand for AI infrastructure has surged globally, with companies investing heavily in data centers, chips, and software platforms to support the rapid growth of generative AI and automation technologies.

Market Implications Highlight Intensifying AI Infrastructure Race

The collaboration underscores intensifying competition in the AI infrastructure space, where major technology companies are racing to build end-to-end ecosystems.

Nvidia, already dominant in AI hardware, is expanding its reach into software and services, while Google continues to strengthen its cloud and AI offerings to compete with other hyperscalers.

For investors, the partnership signals continued momentum in capital spending on AI infrastructure, a key driver of growth for both companies.

At the same time, the scale of investment required raises questions about long-term returns, as companies commit billions of dollars to build out next-generation computing capabilities.

The concept of “AI factories” also reflects a shift toward industrial-scale AI deployment, moving beyond experimental use cases to full-scale integration across industries.

For markets, the deal reinforces a central theme: the AI race is increasingly about ecosystem dominance, with partnerships playing a critical role in shaping the competitive landscape.

Investors will be watching closely to see how quickly these initiatives translate into revenue growth and whether demand for AI infrastructure can sustain its current pace.